Can you maximize your life happiness and relieve financial stress at the same time?

Can you maximize your life happiness and relieve financial stress at the same time?

I believe the answer is yes. The key is practicing radical simplicity.

I’m not about to suggest giving away all of your possessions. Rather, I am suggesting that by being highly intentional in your daily financial decisions, you can increase the odds that what is in your life is truly making your heart sing.

Having less means you have less to take care of. This is true not only of belongings, but for anything that takes up unwanted space in your life. One way to streamline your life is to ask: “Is this object or commitment more important than the time or space it takes up?” If the answer is no, you are on your way to shedding an extraneous layer and getting closer to your own personal definition of radical simplicity.

I believe the same is true when it comes to financial products and services.

The level of complexity in the financial services arena has far exceeded the benefit the vast majority of people are receiving from the plethora of options – whether it’s credit cards, mortgages or investment options.

So how can you use the concept of radical simplicity when it comes to your personal finances?

Recent research by Transamerica’s Center for Retirement Research in conjunction with AEGON reveals that only 15% of workers believe they are on course to achieve the income they want in retirement. Ouch!

So let’s start there. First, spend 15 minutes with a reputable online retirement calculator (like this one from ChooseToSave.org) to determine how much you need to save for the future. The simple awareness of where you are ultimately heading has an amazing power to subconsciously guide you toward smarter daily spending choices.

This step is particularly important for women, who have lower average salaries, spend more time out of the paid workforce, and have longer life expectancies.

According to the MetLife Study of Women, Retirement, and the Extra-Long Life, the average retirement income for women 65 and older in 2009 was 57 percent less than for men of the same age group—$21,519 vs. $37,509. In my work as a women and money expert I’ve seen firsthand how this kind of simple, proactive planning can help close the gap.

Another powerful step you can take is to work with a financial firm that employs a simple, low-fee, straight-forward investment philosophy. At MoneyZen Wealth Management, we love providing this type of financial guidance for clients who meet our $1million minimum. But there are high quality options for women at every net-worth level. Here are several firms I admire that don’t require a 7-figure minimum to be a client:

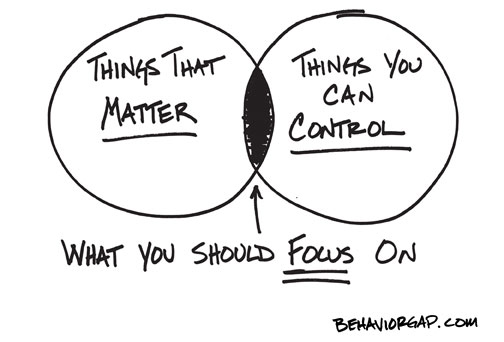

What I like about these firms is that they help you do what my friend, financial author and illustrator Carl Richard’s suggests, which is identify the intersection of what you can control and what is most important. Focusing your financial actions on that sweet spot is an effective way to bring radical simplicity to your money management.

{kind=link}